Carbon credits have gained global attention as a key mechanism for balancing decarbonization and economic activity.

Companies are expected to first reduce their own emissions as much as possible and then use carbon credits to address remaining emissions that are difficult to eliminate. However, what carbon credits are and how they are generated is not always clearly understood, largely due to the complexity of their design.

This article explains the fundamentals of carbon credits, including market types, emissions reduction measurement, credit categories, and the future outlook of the carbon market.

Carbon credits are tradable financial instruments, where one credit represents the reduction or avoidance of one metric ton of CO₂, and they play a critical role in modern climate strategies.

For example, if an afforestation project results in trees absorbing one metric ton of carbon dioxide, that reduction is recognized as one carbon credit.

By purchasing carbon credits, commonly known as carbon offsets, companies can offset their own emissions against verified emission reductions generated elsewhere. In recent years, the importance of carbon credits has increased significantly, as more countries introduce regulations and legislation targeting corporate emissions, and as entire industries become subject to emissions constraints.

Because carbon credits monetize intangible environmental value, such as emission reductions or avoidance, their credibility is underpinned by strict validation and certification processes. Projects that generate carbon credits must be implemented in accordance with project-specific methodologies. Representative standards include Verra’s Verified Carbon Standard (VCS) and the Gold Standard.

In addition, independent third-party entities, known as Validation and Verification Bodies (VVBs), conduct detailed reviews of project design, monitoring systems, baseline calculations, and quantified emission reductions. This multi-layered review process by independent institutions ensures the overall quality and integrity of carbon credits.

Furthermore, mechanisms such as credit retirement systems, which prevent double counting, as well as legal frameworks governing cross-border transfers and eligibility for use, enable carbon credits to be traded with high transparency and real environmental impact.

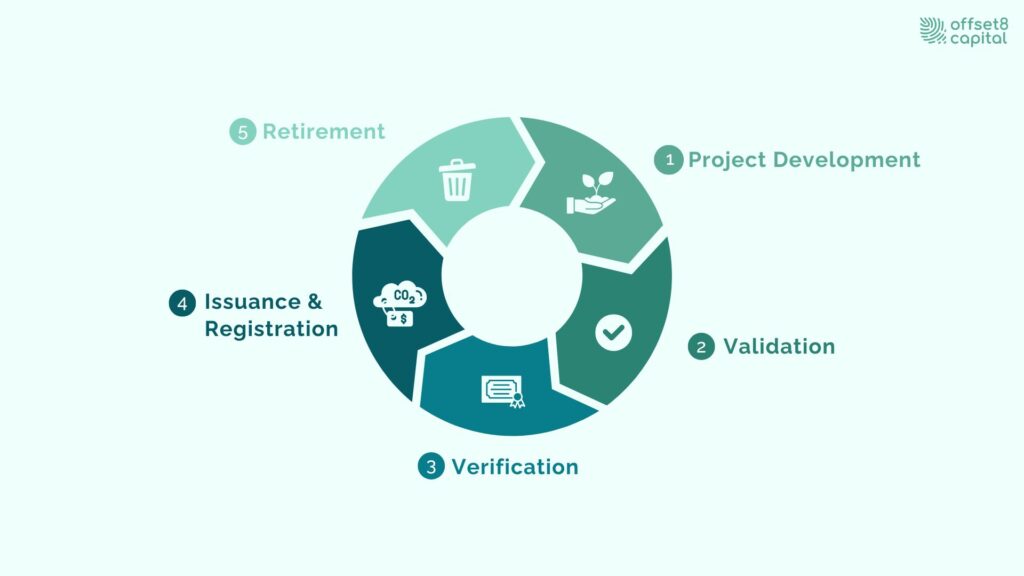

Fig 1: Carbon Credit Lifecycle

Carbon credits are generated through a structured lifecycle that includes methodology selection, project design, project implementation, project validation and verification, certification, issuance, and eventual retirement after use.

The first step is methodology selection, where it is necessary to determine under which scheme the carbon credit project will be implemented. When carbon credits are used under regulations set by governments or international organizations, the types of credits and eligibility criteria are often restricted. In such cases, the project must follow a methodology that complies with the applicable rules. In some instances, no suitable methodology exists for the intended project under a given standard, requiring the development of a new methodology.

Once the methodology is selected, the next step is project design. This involves organizing all information necessary for project implementation, including the project duration, location, scale, and local partners. At this stage, careful attention must be paid, in accordance with the methodology, to the environmental impacts of the carbon credit project, particularly additionality, permanence, and leakage.

Once the project is implemented, audits and data management are conducted in accordance with the MRV (Measurement, Reporting, and Verification) requirements specified in the methodology. At the same time, independent third-party entities known as Validation and Verification Bodies (VVBs) carry out validation and verification. Auditors assess whether the project complies with internationally recognized registry standards and methodologies, thereby ensuring transparency and methodological consistency.

Project progress and status are regularly updated on the registry platform of the standard under which the methodology is issued, allowing public access to project information. After successful verification, the project is registered as verified, carbon credits are issued, and the credits become eligible for trading.

When credits are traded and used, they are retired on the registry platform to prevent double counting. Retired credits are permanently removed from the market and cannot be reused. This mechanism ensures that each credit represents a single, verifiable emission reduction or removal.

The carbon credit market consists of two main segments: the compliance market and the voluntary market.

Compliance Market

The compliance market is a market in which offsetting emissions is mandatory under regulations imposed by governments or international organizations. Companies are required to reduce their emissions in line with regulatory requirements and may also engage in emissions trading and offsetting as part of their compliance strategies.

There are two primary regulatory approaches within the compliance market:

Under both systems, companies may be allowed to offset a certain percentage of their emissions through the purchase of carbon credits. In the compliance market, carbon credits are often used as a means for companies to comply with regulations without significantly scaling back economic activity. While direct emissions reductions remain the top priority, regulatory compliance can sometimes require substantial production cuts, which may sharply increase carbon-related costs. To mitigate such impacts, governments and international organizations seek to stabilize markets by adjusting the allowable offset percentages.

| EU ETS | Launched in 2005, the EU Emissions Trading System is one of the oldest and largest emissions trading schemes in the world. It covers approximately 40 percent of the EU’s total greenhouse gas emissions. |

| CBAM (Carbon Border Adjustment Mechanism) | Starting in 2026, the EU will introduce a mechanism that applies carbon costs to imported goods. This regulation will affect not only companies operating within the EU, but also exporters from other countries, making decarbonization efforts directly relevant to revenue generation. |

| Japan | Japan plans to launch its emissions trading system in 2026. During discussions on system design, proposals were made to allow up to 10 percent of emissions to be offset using carbon credits. Eligible credits are limited to J-Credits generated from domestic projects and JCM credits created in Japan’s partner countries. |

| Singapore | Singapore’s regulatory framework is centered on a carbon tax. At the same time, the country has signed agreements with multiple nations to facilitate the creation of carbon credits overseas, steadily preparing for their future use. |

| South Africa | South Africa also relies primarily on a carbon tax system. While multiple exemption mechanisms have been in place, discussions are currently underway to tighten exemptions and increase the allowable offset ratio using carbon credits to up to 25 percent. |

| CORSIA (Carbon Offsetting and Reduction Scheme for International Aviation) | CORSIA is an international emissions regulation scheme for the aviation sector, led by the International Civil Aviation Organization (ICAO). Strict eligibility criteria apply to carbon credits used for offsetting. As supply remains limited while demand continues to rise rapidly, carbon credit prices under CORSIA have increased significantly. |

Table 1: Examples of Compliance Markets

Voluntary Market

The second segment is the voluntary market. In this market, companies reduce emissions based on self-defined targets rather than legal obligations.

The voluntary market offers a wider range of methodologies and project options, making it relatively easier to participate in. In addition, governments and international organizations may encourage voluntary market activity as a testing phase ahead of the introduction of compliance markets. For companies, the voluntary market also serves as a platform to explore carbon credit use, build internal capacity, and prepare for future regulatory frameworks.

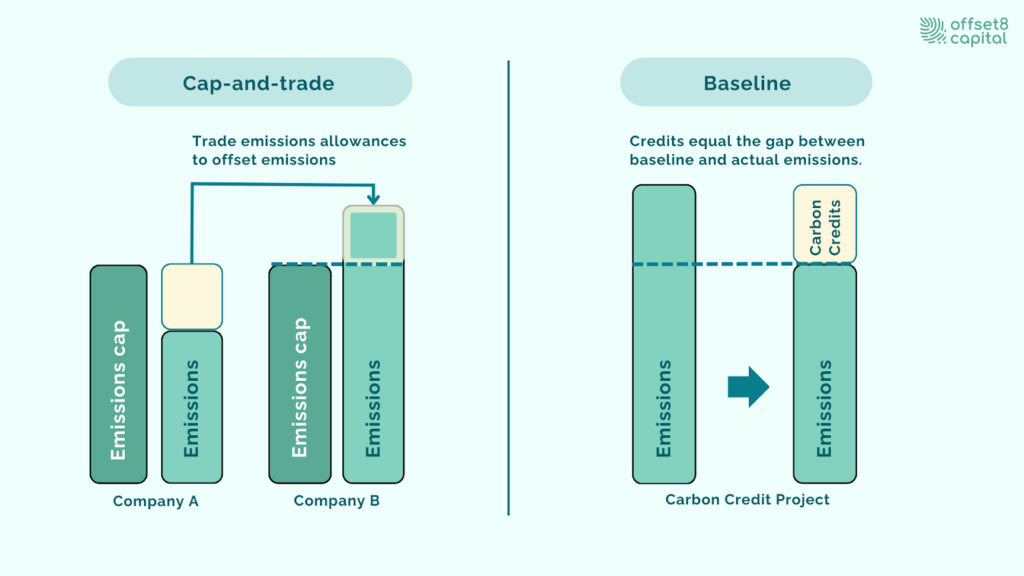

Fig 2: Cap-and-Trade and Baseline

How greenhouse gas emission reductions are defined and quantified depends on the type of system in place. ETS and carbon credit mechanisms differ significantly in how they conceptualize and measure changes in emissions.

Cap-and-trade is a method widely used in ETS. The magnitude of emission reductions is determined by the emissions cap set at the system level. Regulatory authorities at the national or regional level establish an upper limit on total greenhouse gas emissions for covered sectors, and emissions are permitted only within this cap.

Companies are allocated emission allowances. If a company emits less than its allocated amount, it can sell the surplus allowances. If it exceeds its allowance, it must purchase additional allowances from the market. Through this trading mechanism, companies that can reduce emissions at lower cost do so earlier, enabling emissions to be reduced efficiently across the entire system.

In many systems, including the EU ETS, the emissions cap is gradually tightened over time. As a result, emission reduction “change” under an ETS does not reflect the outcome of individual company actions alone, but rather the extent to which the total allowable emissions for society are reduced. Companies must pursue emission reductions and technological transitions in order to continue operating within this framework.

In contrast, under carbon credit mechanisms, emission reductions are measured as the difference relative to a baseline. The baseline represents the level of greenhouse gas emissions that would have occurred in the absence of the project.

Carbon credit quantification first estimates emissions under a “business-as-usual” scenario, assuming no project activity. Actual emissions following project implementation are then measured. The difference between these two values is defined as the emission reduction or removal and is issued as carbon credits.

For example, even if a certain level of CO₂ emissions would have occurred under conventional equipment or agricultural practices, the introduction of energy-efficient technologies or improved farming methods may reduce emissions. That reduction, relative to the baseline, is recognized as a creditable emission reduction. Under this system, emission reduction “change” represents the relative impact generated by a specific project.

Because baseline setting and emission calculations rely on assumptions, carbon credit systems incorporate safeguards such as third-party verification (MRV) and conservative assumptions to ensure the credibility and reliability of quantified emission reductions.

Carbon credits can be broadly categorized into two types: Nature-based Solutions and Technology-based Solutions. Both aim to reduce or remove greenhouse gas emissions, but they differ significantly in their approaches, characteristics, risk profiles, and cost structures.

Nature-based solutions leverage natural systems such as forests, soils, agricultural land, and ecosystems to absorb and store CO₂ or to reduce emissions. These solutions are generally more cost-effective and are well known for generating co-benefits for local communities and the environment.

Representative examples of nature-based projects include:

While nature-based credits are valued for their contributions to biodiversity conservation and improved farmer livelihoods, they also require careful management of risks such as permanence and leakage.

Technology-based solutions use engineering and chemical processes to directly capture, remove, or significantly reduce CO₂ emissions. These approaches typically offer high measurement accuracy and certainty, but tend to involve higher costs.

Representative technology-based projects include:

Technology-based credits are often regarded as having high permanence and reliability, making them particularly important as removal options in the final stages of net-zero pathways. At the same time, challenges remain with respect to technology maturity and the scalability of investments.

Institutional Investment in Carbon Markets

Leading financial institutions such as Morgan Stanley and consultancy firms like BCG project significant demand for high-integrity carbon credits and nature-based solutions.

Investment strategies range from funding project pipelines, participating in forward credit agreements, to integrating carbon offsets into broader ESG frameworks. Institutional flows are helping scale up markets, bringing more transparency, standardization, and liquidity.

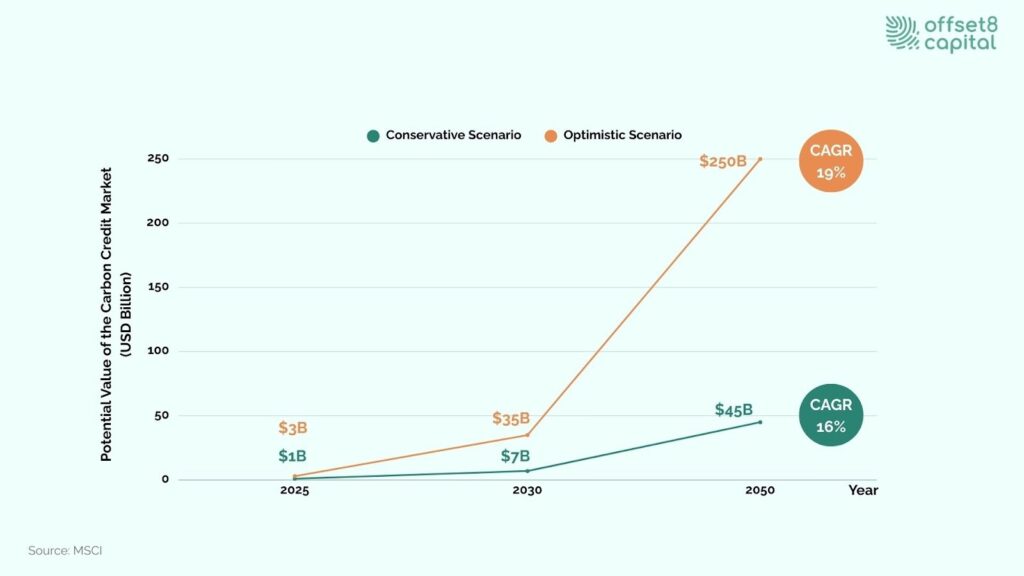

Future Market Projections 2025–2030

Fig 3. Market Growth Projections

The carbon credit market size is expanding rapidly. According to MSCI, the carbon credit market could expand to USD 7 to 35 billion by 2030, supported by stronger corporate climate targets and new policy frameworks. Demand for removal credits, including those from nature-based projects and Direct Air Capture (DAC), is expected to rise sharply.

The market is projected to reach USD 45 billion to 250 billion by 2050. Around two thirds of this value could come from removal credits, with technology-based solutions such as DAC and biochar potentially growing to USD 42 billion.

Key growth drivers include the rapid increase in SBTi-validated corporate targets, the introduction of ICVCM’s Core Carbon Principles (CCPs) to strengthen integrity, and new demand from CORSIA.

Carbon credits are a critical market mechanism that practically supports the transition to a decarbonized society. They serve as a complementary tool that enables organizations to move toward climate targets while maintaining economic activity, particularly in sectors where direct emission reductions are challenging.

The credibility of carbon credits is ensured through rigorous methodologies, third-party verification (MRV), and transparent processes for issuance, trading, and retirement. Across both compliance and voluntary markets, carbon credits play a broad role, from meeting regulatory requirements to preparing for future climate policies.

Looking ahead, demand for high-quality removal credits, including both nature-based and technology-based solutions, is expected to increase significantly. The key is to use carbon credits strategically as a complement to direct emission reductions, rather than as a substitute.

A clear understanding and appropriate use of carbon credits will be essential to strengthening the effectiveness of corporate decarbonization strategies.

Disclaimer

This commentary is for informational purposes only and should not be considered financial, investment, or regulatory advice. Offset8 Capital Limited is regulated by the ADGM FSRA (FSP No. 220178). No assurances or guarantees are made regarding its accuracy or completeness. Views expressed are our own and subject to change

Companies are encouraged to maximize direct emission reductions first and then use carbon credits as a complementary tool to address residual emissions that are difficult to eliminate.

As the market has expanded, the credibility of carbon credits has become a key concern. In response, initiatives such as the ICVCM’s Core Carbon Principles (CCPs) have been introduced to clarify quality standards and strengthen market integrity.

The market is expected to grow, driven by stronger corporate climate targets and new sources of demand such as CORSIA. In particular, the importance of removal-based credits is expected to increase further over time.

The effectiveness of carbon credits depends on their quality. Credits verified under rigorous standards — such as Verra's Verified Carbon Standard (VCS) or the Gold Standard — with robust MRV processes and third-party verification have been shown to deliver measurable, real-world emission reductions. Low-quality credits lacking independent verification, clear baselines, or additionality assessments may not represent genuine reductions. This is why quality standards, transparent methodologies, and independent oversight are central to the credibility and effectiveness of carbon markets.