As demand surges under the Paris Agreement Article 6, Africa still relies on external providers for over 90% of its verification activities. A landmark report by VCMI, GIZ, and Perspectives Climate Group maps the structural challenges and seven strategic pathways that market participants and investors need to watch.

In 2024, Africa accounted for roughly 20% of all new projects listed across the world's leading carbon market registries — a dramatic shift from the continent's historical 3% share under the Clean Development Mechanism. Africa's voluntary carbon credit issuance is now approaching parity with Asia, and the Africa Carbon Markets Initiative (ACMI) projects up to 300 MtCO₂e of annual retirements and USD 6 billion in annual revenue by 2030.

Yet this growth trajectory faces a critical structural constraint: the shortage of Validation and Verification Bodies (VVBs). A comprehensive report published in February 2026 by Perspectives Climate Group, VCMI, and GIZ — "Pathways for Strengthening VVB Capacity in Africa" — systematically analyses this bottleneck for the first time.

This article unpacks the report's key findings, examines the implications for market participants, and outlines the concrete solutions proposed for closing the gap by 2030.

The data presented in the report starkly illustrates the scale of the problem.

Over 90% of verification activities for African projects are carried out by international VVBs and non-African auditors. Of the 48 VVBs accredited by major voluntary carbon market programmes (Verra, Gold Standard, Plan Vivo), only 19 maintain offices in Africa, and most are headquartered outside the continent. Just 9 VVBs have been accredited through African national accreditation bodies, compared to over 170 in Asia and more than 250 in Europe.

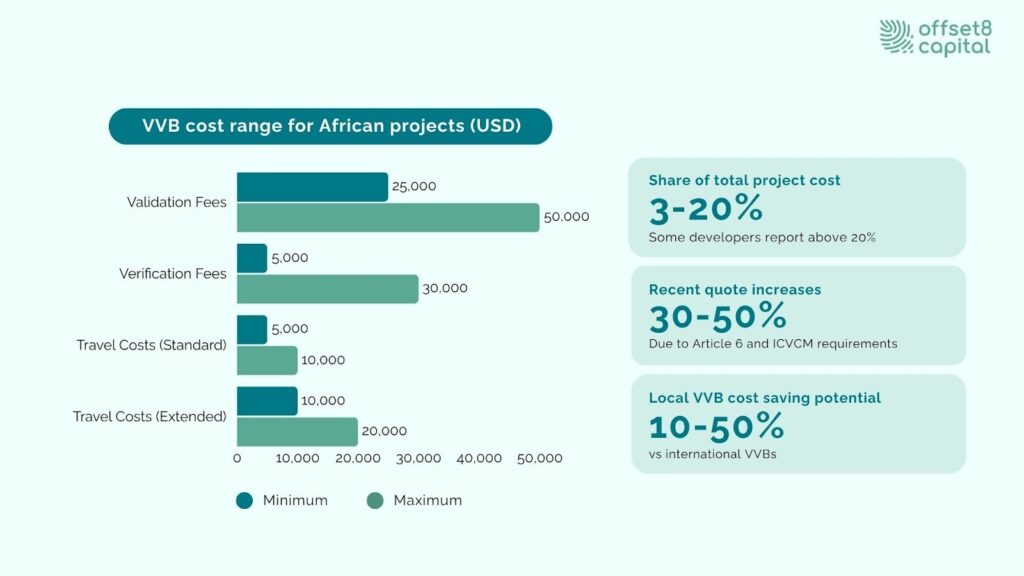

This supply shortage imposes direct economic costs on project developers. Validation fees range from USD 25,000 to 50,000, verification fees from USD 5,000 to 30,000, and international VVB travel costs add a further USD 5,000 to 20,000 per engagement. Developers report that international VVBs can be 10–50% more expensive than local alternatives, with some estimating a premium exceeding 50%, driven largely by travel, logistics, and higher overheads.

Time costs are equally significant. Average validation and verification timelines run 4.5–5 months, with peak delays reaching 9 months — far exceeding the 2–3 month turnaround developers consider ideal. An estimated 10–50% of total project delays and cost overruns are attributable to VVB-related bottlenecks. At the global level, verification-related delays linked to capacity shortages could impose up to USD 2.6 billion in additional costs by 2030.

Fig1: VVB cost range for African projects (USD)

One of the report's most important findings is that VVB capacity constraints are not primarily a training problem. They stem from deeper structural and institutional gaps.

First, policy uncertainty. In many African countries, authorisation procedures under Article 6, corresponding adjustment rules, and institutional mandates remain unclear or in flux. This uncertainty discourages VVBs from making long-term investments in local presence and staffing.

Second, weak MRV systems. Limited availability of high-quality activity data, inconsistent reporting requirements, and underdeveloped domestic MRV frameworks increase the burden on verification teams. Even experienced international VVBs report difficulties operating efficiently in these contexts, resulting in repeated clarification requests and protracted review cycles that drive up costs and timelines.

Third, fragmented accreditation frameworks. Accreditation requirements vary widely across countries, and under Article 6.2 cooperative approaches, VVBs may need to satisfy both buyer-country and host-country accreditation requirements. This duplication further raises market entry costs.

Fourth, poor auditor retention. Demand volatility and limited career progression paths lead trained auditors to leave African carbon markets. Experience from Asia and Latin America confirms that donor-funded training not linked to stable demand fails to produce lasting capacity.

For investors, this structural framing carries a critical implication: VVB constraints represent a systemic risk to Africa's carbon markets, not merely a project-level inconvenience.

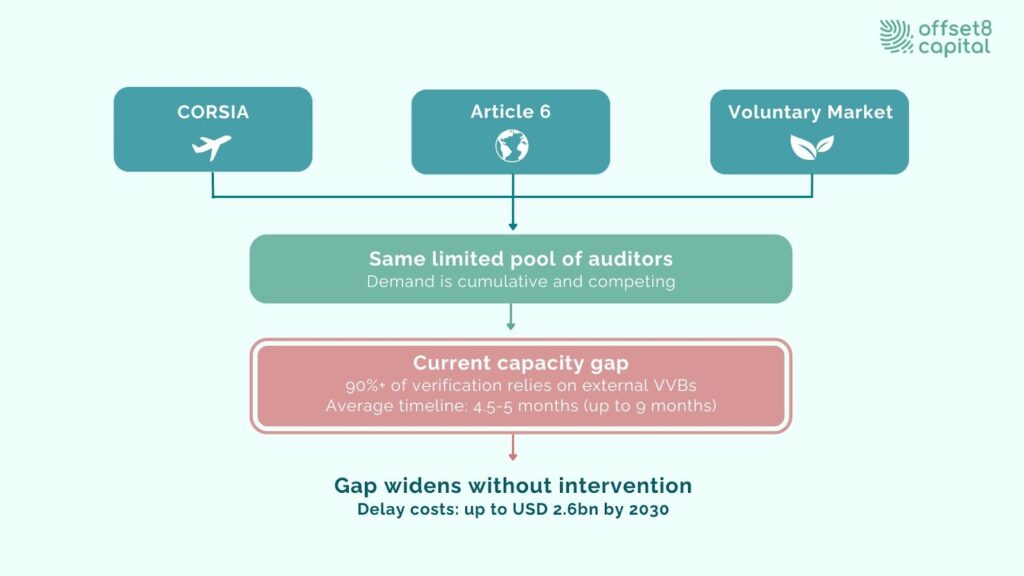

Demand for VVB services is set to expand sharply from multiple market segments simultaneously.

The first driver is CORSIA. Phase 1 (2024–2026) demand is projected at 163 MtCO₂e, rising dramatically to 1,302 MtCO₂e in Phase 2 (2027–2035). For African credits to capture a share of this demand, CORSIA-eligible verification processes are essential.

The second driver is Article 6 cooperative approaches. As of December 2025, 13 African countries had entered into MoUs or bilateral cooperation agreements under Article 6.2. Switzerland, Singapore, Japan, Sweden, and Norway are among the most active buyers. Switzerland alone is implementing or planning 17 activities across Ghana, Senegal, Kenya, Malawi, and Morocco.

The third driver is corporate demand for high-integrity VCM credits. Long-term demand for high-integrity credits to address residual emissions is projected at 4.5 GtCO₂e by 2030 and up to 14 GtCO₂e by 2050. Africa's nature-based mitigation potential remains vastly underutilised — only around 2% is currently harnessed through carbon markets.

Crucially, these demand streams compete for the same limited pool of qualified auditors. Without intervention, the capacity gap will widen, not narrow.

Fig2: Three drivers of VVB demand toward 2030

The report benchmarks Africa against VVB ecosystems in Asia (India, Singapore, Thailand, and others) and Latin America (Brazil, Colombia, Chile, and others).

Markets where sustainable VVB ecosystems have taken root share common features: governments provide clear signals on the role of carbon markets in NDC implementation and formally embed VVB functions within national MRV systems; ISO-aligned national accreditation bodies — such as Brazil's INMETRO, India's NABCB, and Colombia's ONAC — are recognised by major carbon crediting programmes; and sufficient, repeat audit demand enables VVBs to specialise by sector.

Where capacity building has stalled, the pattern is equally consistent: demand uncertainty and volatility deter investment; donor-funded training disconnected from stable market demand produces only temporary results; and trained auditors leave once project cycles end.

The most important lesson for Africa is that training alone does not build durable capacity. Policy clarity, institutional frameworks, and demand predictability must advance in parallel.

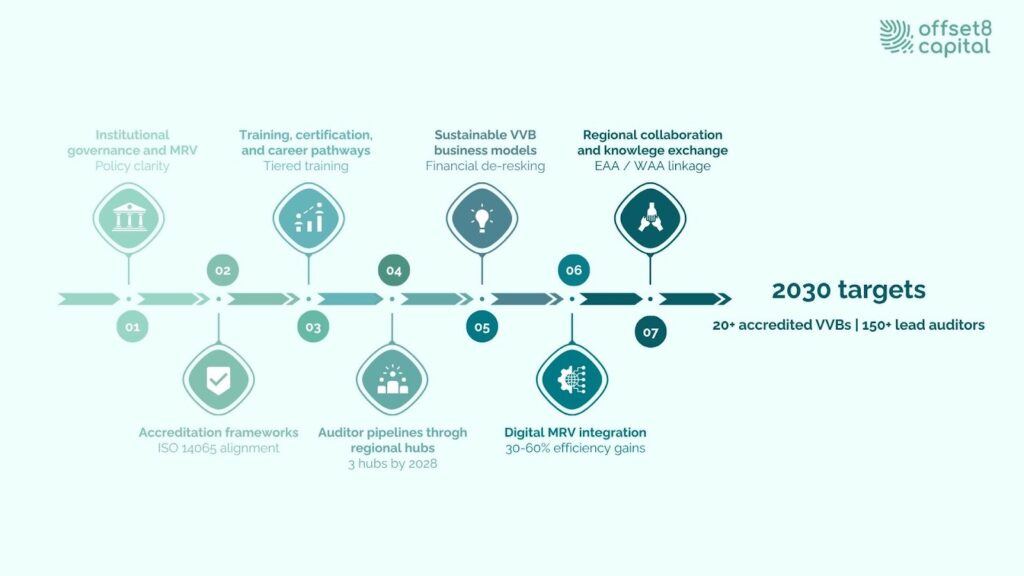

The report proposes seven interconnected pathways for building VVB capacity by 2030.

Fig3: Seven pathways to VVB capacity by 2030

Pathway 1: Strengthen institutional and governance frameworks and MRV functions. Clarifying Article 6 participation rules, authorisation procedures, and corresponding adjustments at the national level is identified as the highest priority. Ghana's Carbon Market Office and Egypt's EGAC are cited as early examples.

Pathway 2: Strengthen accreditation frameworks. Reinforcing national and regional accreditation systems aligned with ISO 14065, and advancing regional harmonisation and mutual recognition through AFRAC, would reduce fragmentation and support cross-border auditor deployment.

Pathway 3: Build structured training, certification, and auditor career pathways. Tiered, competency-based training aligned with ISO 14065 requirements, supported by audit logbooks, peer reviews, and internal competency assessments, would create clear progression routes from trainee to lead auditor.

Pathway 4: Build auditor pipelines through regional training. Establishing at least three regional training hubs by 2028, offering sector-specific programmes and supervised field audits. The West African Alliance on Carbon Markets and Climate Finance (WAA) and a partnership with Saint Louis University in Senegal are among the emerging initiatives.

Pathway 5: Support sustainable and scalable VVB business models. Three complementary models are proposed: independent Africa-based VVBs, regional hub-and-spoke VVBs, and Africa-based audit teams embedded within international VVBs. Targeted financial de-risking — including accreditation cost subsidies, results-based payments, and working capital facilities — is essential.

Pathway 6: Leverage digital MRV to scale verification capacity. Tools such as remote sensing, mobile data collection, and AI-supported data verification could yield significant efficiency gains in audit workflows. However, given limited market readiness and slow regulatory approval cycles, the report recommends gradual integration within robust institutional frameworks.

Pathway 7: Advance regional collaboration and knowledge exchange. Shared training infrastructure, harmonised accreditation processes, and coordinated expert databases — through partnerships with the Eastern Africa Alliance (EAA), WAA, and UNFCCC Regional Collaboration Centres — are identified as necessary enabling conditions.

The report's findings carry several practical implications for carbon market participants.

For project investment due diligence, VVB availability and verification timelines should be explicitly incorporated as risk assessment factors. In technically complex sectors such as AFOLU and blue carbon, verification capacity constraints can directly delay credit issuance.

For buyers considering Article 6 credits, the maturity of host-country accreditation frameworks and VVB availability are critical factors determining transaction feasibility. Countries such as Ghana already require local expert participation in audit teams, meaning local VVB capacity directly affects project selection.

For firms considering VVB market entry, Africa offers significant first-mover advantages, but accreditation costs (USD 50,000–60,000), quality assurance systems, and specialist recruitment require substantial upfront investment. Donor support and blended finance represent the most realistic entry strategies.

COP32, to be held in Addis Ababa, Ethiopia, in 2027, is widely recognised as an "African COP" and represents a critical opportunity to elevate Africa's carbon market challenges — including VVB capacity strengthening — onto the international agenda.

Beyond its analytical contribution, the report has informed the design of a strategic VVB accelerator programme concept that combines policy engagement, accreditation-aligned training, supervised audit deployment, and targeted financial support to unlock private investment in Africa-based VVB capacity.

Africa has both the technical talent and the market potential. The challenge is not training alone, but aligning demand with capacity through clear policy signals, credible MRV systems, coordinated accreditation frameworks, and targeted investment. Confronting this structural challenge head-on is the prerequisite for Africa to become a competitive supplier of high-integrity carbon credits on the global stage.

Disclaimer

This commentary is for informational purposes only and should not be considered financial, investment, or regulatory advice. Offset8 Capital Limited is regulated by the ADGM FSRA (FSP No. 220178). No assurances or guarantees are made regarding its accuracy or completeness. Views expressed are our own and subject to change

Prolonged verification timelines (averaging 4.5–5 months, up to 9 months) directly delay credit issuance, and an estimated 10–50% of project delays and cost overruns are attributed to VVB-related bottlenecks. Investors should explicitly incorporate VVB availability and verification timelines into their due diligence risk assessments.

Digital MRV can improve audit workflow efficiency but does not address the root causes. Structural challenges such as policy uncertainty and fragmented accreditation frameworks cannot be resolved by technology alone — the report positions digital MRV as a complementary tool to be gradually integrated within robust institutional frameworks.

The report sets targets of at least 150 accredited African lead auditors and 20 or more accredited VVB entities by 2030, and concludes that meaningful improvement is achievable with appropriate intervention. However, training alone is insufficient — policy clarification, regional accreditation harmonisation, financial de-risking, and auditor career pathway development must advance simultaneously.