Japan's climate strategy is built on a distinctive approach that combines industrial policy, phased regulatory tightening, and targeted fiscal support. Rather than imposing abrupt mandates, the government first built out market infrastructure, embedded carbon pricing through voluntary participation, and is progressively strengthening obligations as institutional capacity matures.

At the core of this strategy is the GX-ETS (Emissions Trading System), which became mandatory in April 2026. It applies to operators whose average annual direct CO₂ emissions over FY2023–FY2025 exceed 100,000 tonnes. Together, these companies account for approximately 60% of Japan's total greenhouse gas emissions.

Underpinning the ETS is the GX (Green Transformation) Promotion Strategy, which targets over ¥150 trillion (approximately USD 1 trillion) in public and private climate-related investment over the next decade. As an initial tranche, a ¥20 trillion (approximately USD 135 billion) front-loaded investment package financed through GX Economy Transition Bonds is already underway.

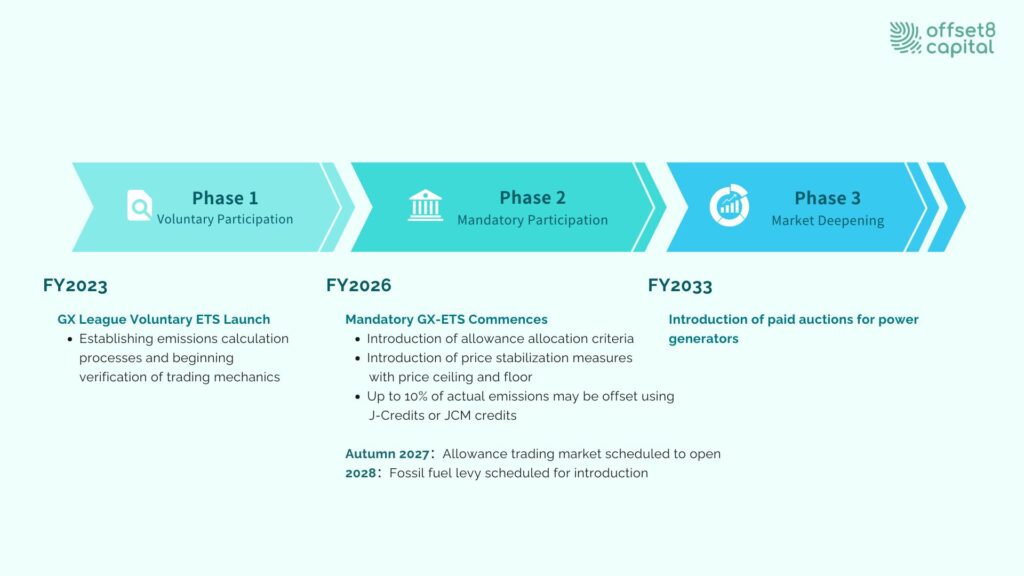

Fig 1: GX-ETS Implementation Timeline

Japan's carbon market has built its institutional foundations through a series of clearly defined phases.

GX-ETS launched in April 2023 as a voluntary scheme under the GX League framework, with over 700 participating companies covering more than 50% of Japan's domestic GHG emissions. This phase served as an operational trial period in which companies established emissions calculation processes, tested trading mechanics, and began adapting to third-party verification requirements. A surplus reduction allowance mechanism was also introduced, enabling companies that exceeded their voluntary targets to trade surplus credits.

Following the passage of the revised GX Promotion Act in May 2025, the ETS transitioned to a mandatory compliance regime in April 2026. Key features of this seven-year phase include allowance holding obligations, allocation criteria based on government guidelines, third-party verification by registered verification bodies, and price stabilization measures including price ceilings and floors. The allowance trading market, to be operated by the GX Acceleration Agency, is scheduled to open in autumn 2027.

From FY2033, paid auctions will be introduced for power generators, establishing a full carbon price discovery mechanism and enabling gradual alignment with international carbon pricing levels.

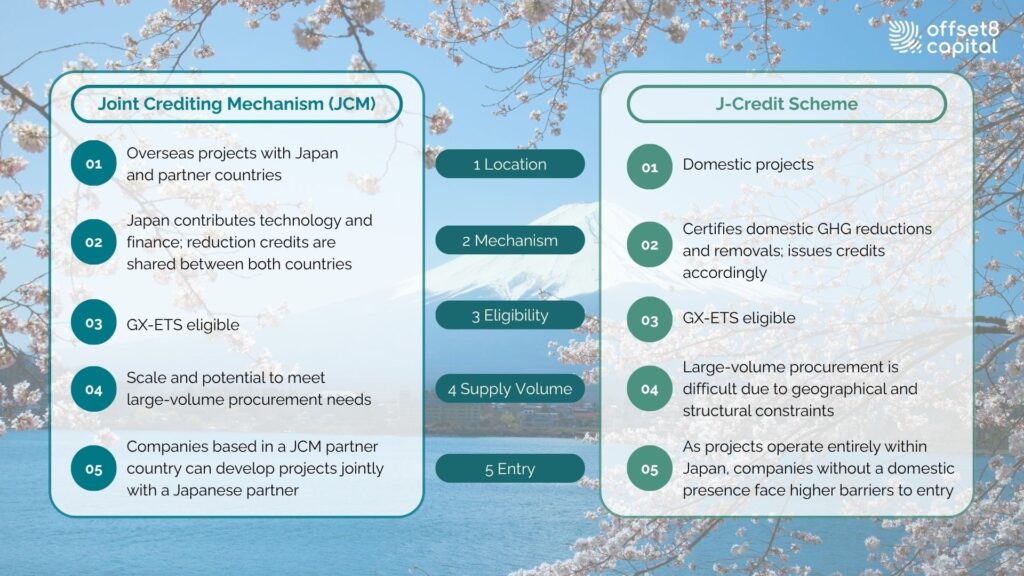

Japan's carbon credit framework has developed around two pillars: the J-Credit Scheme for domestic projects, and the Joint Crediting Mechanism (JCM) for cooperation with partner countries.

2006: The Act on Promotion of Global Warming Countermeasures mandated GHG emissions calculation and reporting for large emitters (specified emitters), establishing Japan's foundational emissions data infrastructure.

2008: Two parallel schemes launched. The J-VER (Japan Verified Emission Reduction) scheme targeted voluntary carbon offsets by SMEs and local governments. The Domestic Credit Scheme enabled large corporations to support GHG reduction activities by SMEs and apply the results toward their own targets.

2011: Negotiations on the JCM (Joint Crediting Mechanism) began — an international framework under which Japan and partner countries jointly implement GHG reduction projects and share the resulting credits.

2013: J-VER and the Domestic Credit Scheme were consolidated into the unified J-Credit Scheme, with joint administration established across the Ministry of Economy, Trade and Industry (METI), the Ministry of the Environment (MOE), and the Ministry of Agriculture, Forestry and Fisheries (MAFF).

2023: A voluntary ETS launched under the GX League, introducing surplus reduction allowances. In October, the Tokyo Stock Exchange (JPX) opened a carbon credit market for J-Credit trading.

2025: Tokyo Metropolitan Government launched the Tokyo Carbon Credit Market, adding international voluntary carbon credits (VCCs) alongside J-Credits. The revised GX Promotion Act passed in May, and in December the Industrial Structure Council's ETS Subcommittee published an interim report finalizing the technical details of allocation guidelines.

2026: The mandatory GX-ETS commenced. For compliance purposes, operators may offset up to 10% of their reported emissions using J-Credits or JCM credits.

The December 2025 interim report by the ETS Subcommittee finalized the allocation framework for the mandatory ETS. Allowances are allocated under two methods: benchmarking and grandfathering (GF).

The benchmark method applies to energy-intensive sectors where cross-industry comparison is feasible, including oil refining, steel, chemicals, and cement. Allocations are calculated by multiplying the three-year average production volume (FY2023–FY2025) by a sector-specific benchmark value. That benchmark tightens linearly from the top 50th percentile in the base year to the top 32.5th percentile by FY2030. Sectors with significant deviation from the benchmark are subject to a five-year transitional relief measure at the start of the scheme.

The grandfathering method applies to sectors where benchmarking is not feasible. Allocations are derived by applying an annual reduction rate to the three-year average baseline emissions: 1.7% per year for energy-derived CO₂, and 0.3% per year for process-derived CO₂ where structural abatement options are limited.

Three adjustment mechanisms are also built into the allocation framework:

| Adjustment Measure | Trigger Condition | Additional Allocation |

| Recognition of early reduction efforts | GF-covered sources with verified reductions exceeding the GF rate | Excess reduction reflected (activity-level adjustment factor of 0.8 applied) |

| Carbon leakage mitigation | Trade intensity > 0.1 AND allowance procurement costs > 4% of operating profit | 50% of shortfall |

| GX R&D investment recognition | Prior-year GX-related R&D expenditure | Approx. 10–20% of shortfall |

Table 1: Allowance Adjustment Measures

The ETS operates within a price corridor — a ceiling and floor set annually by the Minister of Economy, Trade and Industry:

| FY | Price Ceiling (¥/tCO₂) | Ceiling (ref. USD/tCO₂) | Price Floor (¥/tCO₂) | Floor (ref. USD/tCO₂) |

| 2026 | 4,300 | 28.7 | 1,700 | 11.3 |

| 2027 | 4,429 | 29.5 | 1,751 | 11.7 |

| 2028 | 4,562 | 30.4 | 1,804 | 12.0 |

| 2029 | 4,699 | 31.3 | 1,858 | 12.4 |

| 2030 | 4,840 | 32.3 | 1,913 | 12.8 |

Table 2: ETS Price Ceiling and Floor (at ¥150/USD)

*Figures for FY2027 onward are reference projections based on estimates as of 2025. Actual prices are re-determined and officially announced annually by METI based on that year's inflation forecast, and may differ from the figures shown.

Both ceiling and floor increase at approximately 3% per year. The price corridor is designed to ensure market stability and regulatory effectiveness.

This price corridor also serves as a reference benchmark for investment in J-Credit and JCM projects. However, where actual project development costs exceed the allowance price, this may pose a viability barrier — a consideration that warrants careful attention.

Reporting of actual emissions and applications for allowance allocation require confirmation by a verification body registered with the Minister of Economy, Trade and Industry. The verification regime is designed to become progressively more rigorous:

Requirements for registered verification bodies will also be raised over time. Initial eligibility is based on experience in emissions assurance and verification for listed companies, with future requirements expected to include ISO 14065 accreditation and sustainability assurance qualifications.

Covered operators are required to prepare, submit, and publish an annual transition plan covering:

The allowance trading market, to be established and operated by the GX Acceleration Agency, is scheduled to open in autumn 2027. Participants will include covered operators as well as dealers with carbon credit trading experience, such as market makers. The market's core functions encompass settlement, publication of trading information, and ensuring fair trading practices.

Market activation measures — drawing on lessons from the EU ETS and South Korea's K-ETS — are under consideration for FY2026, including:

In the EU and Korean markets, trading has historically been concentrated in narrow windows, resulting in periodic liquidity shortfalls. Japan faces analogous risks and will need to address them proactively.

Japan's carbon credit framework rests on two pillars: J-Credits generated by domestic projects, and JCM credits generated by projects in partner countries. Under GX-ETS, operators may offset up to 10% of their reported emissions using J-Credits or JCM credits.

Fig 2: Comparison of JCM and J-Credit Schemes

JCM is a bilateral framework under which Japan partners with other countries to implement GHG reduction and carbon removal projects, distributing the resulting credits between both parties. Japan provides low-carbon technologies, expertise, and finance to support emissions reductions in partner countries. Credits generated can be used by both governments toward their Nationally Determined Contributions (NDCs) under Article 6 of the Paris Agreement.

| Region | Countries | n |

| Africa | Ethiopia, Kenya, Tanzania, Senegal, Tunisia | 5 |

| Asia | Mongolia, Bangladesh, Maldives, Vietnam, Laos, Indonesia, Cambodia, Myanmar, Thailand, Philippines, Sri Lanka, Uzbekistan, Kyrgyz Republic, Kazakhstan, India | 15 |

| Middle East & West Asia | Saudi Arabia, UAE, Oman, Azerbaijan, Georgia | 5 |

| Americas | Costa Rica, Mexico, Chile | 3 |

| Europe | Moldova, Ukraine | 2 |

| Oceania | Palau, Papua New Guinea | 2 |

| Total | 32 | |

Table 3: JCM Partner Countries (32 countries as of June 2026)

The scheme is administered by the JCM Implementation Authority (JCMA), formally established under the revised Act on Promotion of Global Warming Countermeasures in April 2025. The operating body is the Global Environment Centre Foundation (GEC), which oversees project registration, credit issuance, and coordination with partner countries.

The J-Credit Scheme certifies GHG reductions and removals achieved through domestic projects. It is jointly administered by METI, MOE, and MAFF, and is widely used by Japanese companies and local governments.

Government target: Based on the Global Warming Countermeasures Plan adopted by Cabinet in October 2021, Japan aims to certify a cumulative total of 15 million tonnes by FY2030.

Project types:

Domestic J-Credits alone are unlikely to meet full compliance needs due to geographical and structural supply constraints, making JCM the primary pathway for large-volume procurement. That said, given current low allowance prices, the gap between JCM project development costs and prevailing market prices can itself be a barrier to entry. A strategic approach — combining available subsidies with co-investment arrangements — is essential when evaluating project participation.

Opened by the Tokyo Stock Exchange on 11 October 2023. Current tradable instruments are limited to J-Credits. Eligible participants are restricted to corporations, government bodies and local authorities, and incorporated associations — and as of 2026, registration is limited to Japan-domiciled entities only.

A platform launched by the Tokyo Metropolitan Government in 2025. In addition to J-Credits, international voluntary carbon credits (VCCs) are also tradable. The platform is designed with a particular focus on supporting SMEs through their decarbonization transition.

Both platforms contribute to market transparency by improving price visibility and clarifying market mechanics. When the allowance trading market opens in autumn 2027, the relationship between the credit markets and the allowance market is expected to become considerably clearer.

This section outlines key action points for businesses and critical perspectives for investors.

Emissions Management and Credit Utilization for Companies

The first priority for companies is to accurately measure their GHG emissions.

Since April 2006, under the Act on Promotion of Global Warming Countermeasures, Japan’s Ministry of the Environment has required designated emitters — businesses that emit GHGs above a certain threshold — to calculate and report their emissions to the government.

Even for companies not currently subject to this regulation, it is highly advisable to begin voluntary emissions tracking in anticipation of future regulatory requirements. Guidance on reporting procedures and technical requirements is available through the Ministry of the Environment’s official documentation.

How Carbon Market Could Impact Investment Volatility in Japan

For investors, it is essential to closely monitor developments in emissions trading schemes (ETS). In particular, the following factors can significantly impact portfolio risk and return:

One promising area of opportunity is direct investment in carbon removal projects and clean energy initiatives. Projects and funds linked to JCM and J-Credit Scheme are especially noteworthy, given their strong ties to Japan’s domestic carbon market and the anticipated growth in credit demand in the years ahead.

Securing High-Quality Credits and Managing Risk

Japan is entering Phase 2 of its carbon market, marking the start of its national ETS. This phase introduces a penalty-based mechanism, where companies face financial consequences for excess emissions.

Initially, regulations will focus on large-scale emitters — particularly in the energy sector — but will gradually expand to other industries. In a recent meeting hosted by the Ministry of the Environment, the government announced a policy allowing up to 10% of emissions to be offset using J-Credits or JCM credits. Although this cap may change in the future, the need for companies to incorporate credits into their compliance strategy is inevitable.

Credit Price Volatility and the Importance of Early Action for Climate Goals

Carbon credit prices are highly sensitive to changes in supply and demand. Demand spikes — especially around regulatory enforcement or ETS rollout — can drive rapid price increases. There is a real risk that credits may become prohibitively expensive right when companies need them most.

A relevant example is CORSIA (Carbon Offsetting and Reduction Scheme for International Aviation), a global framework introduced by ICAO (International Civil Aviation Organization).

Under CORSIA, airlines are required to offset emissions using only CORSIA-eligible credits, which meet strict environmental criteria.

Due to limited supply and rapidly growing demand from international carriers, credit prices have surged, and further increases are expected. This type of market pressure could easily occur in Japan as well. For instance, risks such as the expansion of the ETS, a reduction in allowable offset percentages, or sudden policy shifts could all trigger a surge in credit demand.

Any of these factors could trigger a scramble for credits, leading to dramatic price spikes.

Therefore, it is vital that both companies and investors develop forward-looking strategies for credit procurement and portfolio planning now, before market conditions tighten.

Assessing Credit Quality and Avoiding Greenwashing

While low-cost credits may seem attractive, it is crucial to verify their legitimacy and environmental integrity. Buyers should evaluate:

Careful due diligence helps companies avoid reputational damage and accusations of greenwashing — claiming to be environmentally responsible without real impact. Securing high-quality credits not only enhances environmental outcomes but also strengthens corporate credibility and mitigates reputation-related risks.

Offset8 is a global emissions investment and management group founded in Abu Dhabi, United Arab Emirates. At COP28, Offset8 announced the Middle East's first carbon market fund with target size of $250m.

Offset8 seeks to finance nature-based solutions in Africa and Southeast Asia, as well as provides financing in the form of prepayments and offtake contracts for the delivery of verified carbon credits, with subsequent sale of the carbon credits under compliance markets (e.g., CORSIA and regional ETS), Article 6 of the Paris Agreement or voluntary purposes.

Offset8 Capital has an existing pipeline of approximately 70 projects: the investment portfolio includes such projects as CORSIA-eligible iRise (Malawi's largest reforestation and clean cooking program), Sawa (Indonesia's largest biochar carbon removal project), and others. These projects undergo rigorous verification, ensuring institutional investors receive premium carbon credits that meet evolving regulatory requirements. Our commitment to carbon neutrality across Scope 1, 2, and 3 emissions aligns with Science-Based Targets initiative requirements, demonstrating institutional leadership while providing credible expertise for client engagement on climate strategy development.

We work closely with Japanese companies on their decarbonization efforts, drawing on global experience and local networks. Our bilingual team provides end-to-end support, from project design and certification to credit issuance and market entry. We cover key mechanisms including AWD, biochar, Article 6 of the Paris Agreement, and CORSIA. As Japan’s carbon market evolves, Offset8 Capital offers strategic, globally informed support to help companies lead in the climate transition toward net zero.

Disclaimer

*Disclaimer: This commentary is for informational purposes only and should not be considered financial, investment, or regulatory advice. No assurances or guarantees are made regarding its accuracy or completeness. Views expressed are our own and subject to change

Japan's national emissions trading system (ETS) began full operation in April 2026. Preparatory initiatives, such as the GX League and carbon credit trading platforms, had already been underway in the years prior.

J-Credits are issued by the Japanese government for verified emission reductions or removals within Japan. JCM credits, on the other hand, are generated through bilateral projects between Japan and developing countries under the Joint Crediting Mechanism

As Japan’s national emissions trading system launches in 2026, foreign companies can partner with local players on climate projects or fund emissions reduction initiatives. Early entry helps shape market practices and tap into rising demand for credible credits.