Agriculture is both a significant source of greenhouse gas (GHG) emissions and one of the few sectors with the potential to absorb and store carbon. In particular, soil organic carbon (SOC) has gained international attention as a key lever that can simultaneously support climate change mitigation and improvements in agricultural productivity.

Against this backdrop, Verra developed VM0042 Improved Agricultural Land Management (IALM) under the Verified Carbon Standard (VCS) program. This article provides a structured overview of the methodology, focusing on the latest v2.2, which became active on 21 October 2025, including its core concepts, applicability conditions, quantification approaches, and practical implementation considerations.

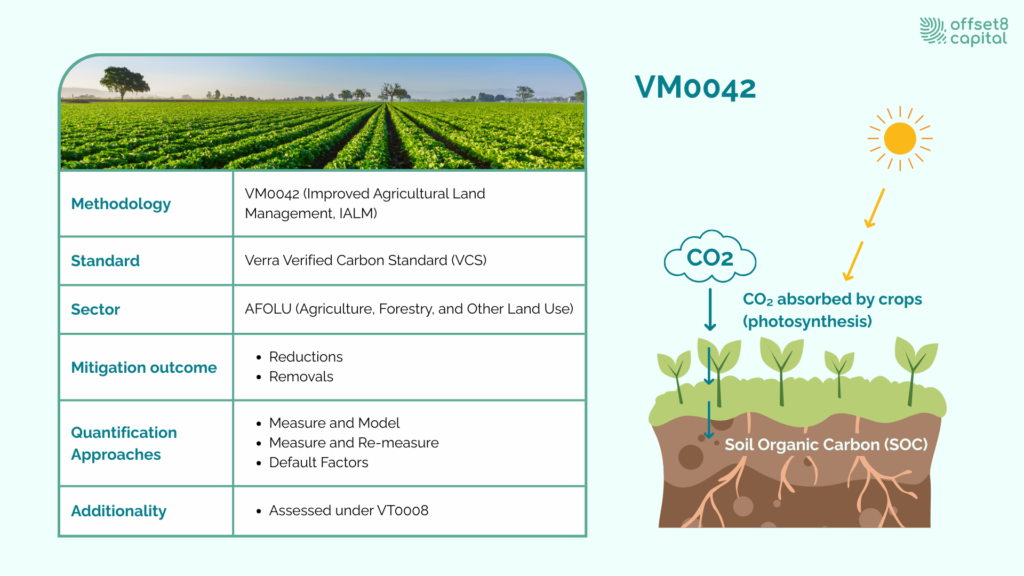

Fig1: VM0042 | How Improved Agricultural Land Management Generates Soil Carbon Credits

VM0042 (Improved Agricultural Land Management) is a methodology designed to quantify GHG emission reductions and carbon removals achieved through improvements in on-the-ground agricultural land management practices. It covers both:

A defining feature of VM0042 is that it does not stop at emission reduction accounting. It effectively treats farmland as a carbon-storing asset, reflecting the idea that day-to-day management decisions - such as reducing tillage, optimizing fertilization and water management, or introducing cover crops and crop rotations - can contribute to long-term increases in SOC stocks.

The applicable land-use categories are limited to cropland and grassland, but the methodology is not restricted to specific regions or climate zones.

In VM0042, SOC is positioned as the central carbon pool for quantification. SOC is treated as a mandatory carbon pool and cannot be excluded as de minimis, even in cases where other methodologies might allow certain pools to be excluded. This design choice clearly shows that VM0042 places SOC stock change at the core of quantification.

In addition, VM0042 includes CO₂, CH₄, and N₂O emissions originating from agricultural activities as key contributors to the overall project quantification. In other words, VM0042 provides a framework that captures both SOC stock change and major agricultural GHG emission sources affected by land management improvements.

VM0042 has been updated over time to reflect practical experience and evolving scientific knowledge. The first release, v1.0 (2020), was developed by TerraCarbon and Indigo Ag and is often viewed as an early, foundational methodology that formally connected regenerative agriculture practices with soil carbon crediting.

Subsequent versions, v2.0 and v2.1, were led by Verra and included revisions, particularly to sections related to uncertainty, aimed at strengthening both scientific robustness and market credibility.

The current version, v2.2 (active as of October 2025), can be understood as a consolidated update that builds on earlier revisions. Key areas of refinement include clearer requirements for model-based quantification, more structured treatment of SOC measurement options (including direct measurement and proximal sensing), and expanded practical guidance for project developers.

As a result, v2.2 has evolved into a methodology that better balances flexibility with rigor, aligning more closely with market demand for high-quality agricultural carbon credits.

To apply VM0042, a project must demonstrate that material improvements in agricultural land management have been implemented relative to pre-project practices. The methodology anticipates not only single interventions but also project designs that combine multiple improvement measures.

Eligible measures include, for example, enhanced fertilizer management, improved water and irrigation practices, reduced tillage and optimized residue management, improvements in planting and harvesting practices including cover cropping and crop rotation, and improved grazing management. A non-exhaustive list is provided in Appendix 1.

Importantly, these changes must not be merely qualitative. They must also represent meaningful quantitative improvements. For instance, where fertilizer reductions are claimed, the methodology requires changes that exceed a defined threshold (for example, changes that exceed defined materiality thresholds (often illustrated as changes greater than 5% relative to historical management levels). These requirements help prevent business-as-usual practices from being over-credited.

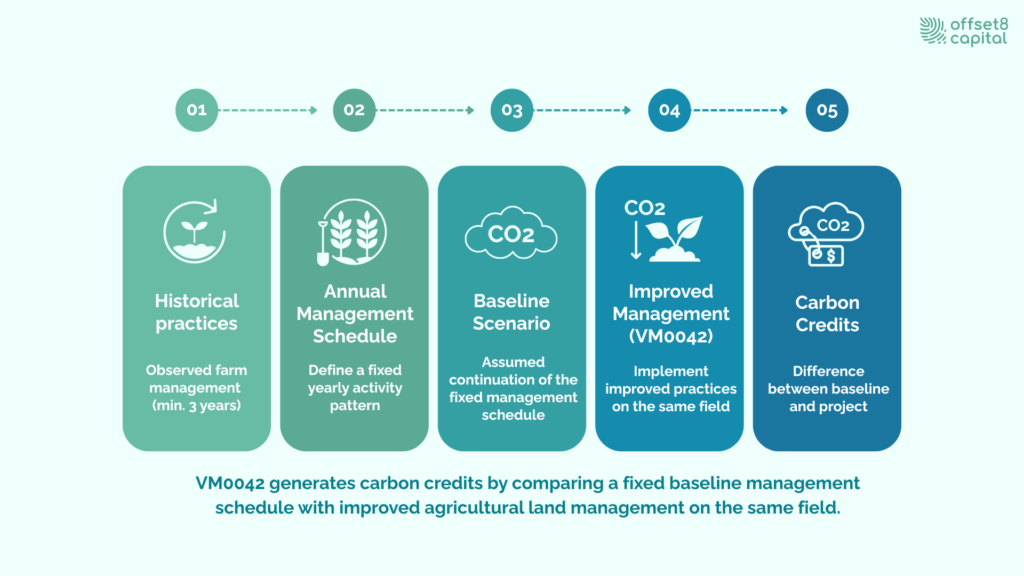

Fig2: How Carbon Credits Are Generated under VM0042

In VM0042, the baseline can be summarized as the continuation of the agricultural land management (ALM) practices that were implemented prior to the project start date. A key point is that the baseline is not an abstract regional average. It is reconstructed as field-level, verifiable management actions at the level of each quantification unit.

To do so, VM0042 requires organizing pre-project practices - such as cropping, fertilization, tillage, irrigation, harvesting, and residue management - into an annual Schedule of Activities. This step effectively locks in what happens each year under the baseline in a way that can be validated and verified.

Minimum 3-Year Historical Look-Back and Treatment of Cropping Systems

The historical period (x years) used to develop the Schedule of Activities must be at least three years. In areas where crop rotations are practiced, the selected period must include at least one full rotation cycle. This is because a single-year snapshot may not reflect cyclical patterns in rotations and management, potentially distorting the baseline definition.

Once defined, the schedule is applied repeatedly over the baseline period in x-year cycles (for example, a three-year pattern of tillage or non-tillage and fertilizer timing is repeated as-is). This structure helps prevent arbitrary baseline changes and provides consistent assumptions for both model-based quantification (Approach 1) and direct measurement approaches involving baseline control sites (Approach 2).

VM0042 applies a Project Method approach to additionality. Rather than relying solely on observed reductions, this framework requires explaining why the improvements would not have occurred without carbon credit revenue.

The first step is confirming Regulatory Surplus, meaning that the proposed practices are not already required by laws or regulations.

The second step is Barrier Analysis, which must be conducted in accordance with Step 2 of the most recent version of VT0008 (Additionality Assessment). This analysis identifies and evaluates financial, informational, technological, and institutional barriers that prevent the adoption of the proposed practices under business-as-usual conditions. In practice, these barriers often include high upfront investment requirements, limited technical know-how or operational capacity, and risk-averse farming practices. The objective is to demonstrate that, while the measures may be technically viable or economically beneficial in theory, they are unlikely to be implemented or scaled without the additional incentive provided by carbon credit revenues.

The third step is Common Practice Analysis, which examines how widely similar improvements have already been adopted in the relevant region. As a general rule, the adoption rate should be below 20%. Even where adoption exceeds 20%, additionality may still be demonstrated if the reasons for adoption differ materially, such as heavy reliance on grants or non-commercial financing.

Together, these three steps enable VM0042 additionality assessments to be grounded in both numerical evidence and real-world sector conditions.

VM0042 provides three quantification approaches. Project proponents select an approach based on the type of emissions or removals, data availability, and project scale.

Approach 1: Measure and Model uses a biogeochemical process-based model to estimate SOC change and GHG fluxes. It is well suited to large-scale, long-term projects. Under this approach, SOC must be measured at least every 5 years to support model true-up.

Approach 2: Measure and Re-Measure quantifies SOC stock change through direct measurement. This approach is relevant where models are unavailable or not sufficiently validated for a particular region, crop, or practice, or where proponents prefer direct measurement. However, it requires linked baseline control sites that continue baseline management, which increases design and operational complexity.

Approach 3: Default Factors uses IPCC-based default emission factors for specific sources. It is supplementary and limited in scope, but can be a practical option for certain emissions sources where applicable.

In all cases, within the same quantification unit, the baseline and project scenarios must use the same quantification approach. This is a point that requires careful attention during validation and verification.

At the core of VM0042 MRV (Monitoring, Reporting, and Verification) is the measurement and management of SOC. Because SOC is treated as a mandatory carbon pool, measurement accuracy and uncertainty management materially affect credit integrity.

A key requirement is the use of stratified random sampling. SOC varies substantially across cropland and grassland due to factors such as soil type, topography, historical land use, and management history. Treating the entire project area as uniform risks systematically over- or under-estimating SOC changes in certain conditions.

Stratified sampling addresses this heterogeneity by dividing the project area into relatively homogeneous strata and then selecting sampling points randomly within each stratum. This improves sampling efficiency and reduces errors, thereby supporting lower uncertainty and better explainability at verification.

For SOC measurement itself, VM0042 allows both conventional laboratory methods (for example, dry combustion) and proximal sensing techniques such as INS, LIBS, MIR, and Vis-NIR. Regardless of the method used, project proponents must be able to consistently demonstrate measurement accuracy, sampling design integrity, and QA/QC procedures.

One common source of confusion in practice is how VM0042 relates to biochar. In short, biochar application itself is not eligible as a project activity under VM0042. If the goal is to generate biochar-only removal credits, a dedicated biochar methodology is typically the appropriate route.

That said, there is often strong practical demand to use biochar as a soil amendment in agricultural settings. Under VM0042, the key is to avoid double-counting, meaning not treating externally added stable carbon (biochar) as if it were purely an SOC increase driven by land management improvements. Where biochar is applied, any SOC stock change directly attributable to the added biochar carbon must be accounted for appropriately so that credited SOC increases do not simply reflect carbon that was imported into the soil system.

For projects that combine VM0042 with other methodologies, especially those related to biochar or biomass and vegetation carbon, clear allocation of credited carbon and early identification of double-counting risks are essential. During verification, the question of what is being credited under which methodology will be scrutinized, so a clean division of roles between methodologies can materially affect audit defensibility and overall project feasibility.

VM0042 is notable for positioning agriculture not only as an emissions source, but as a sector that can meaningfully contribute to climate mitigation through measurable improvements in land management. Few methodologies connect long-term soil health improvements and carbon storage to internationally recognized, MRV-based carbon credits with comparable rigor.

VM0042 also matters because it can align climate mitigation with resilient food production. SOC improvements can support productivity stability and climate resilience, making the practices potentially rational from a farm business perspective. Adding carbon credit revenue can further expand the space for incentive design in the agricultural economy.

At the same time, VM0042 is not a lightweight methodology. Its SOC-centric MRV requirements are demanding, and meaningful costs and specialized capabilities are needed for baseline development, data management, and verification readiness. For that reason, VM0042 is best seen as a framework for proponents who prioritize certainty and long-term value creation over short-term credit volume.

Overall, VM0042 is a strategic option for medium-to-large agricultural projects and for companies and investors seeking high-integrity agricultural carbon credits that connect farming and climate action in a measurable and verifiable way.

Disclaimer

This commentary is for informational purposes only and should not be considered financial, investment, or regulatory advice. Offset8 Capital Limited is regulated by the ADGM FSRA (FSP No. 220178). No assurances or guarantees are made regarding its accuracy or completeness. Views expressed are our own and subject to change

VM0042 is Verra VCS’s methodology for agricultural projects that quantify and credit GHG emission reductions and carbon removals achieved through improved agricultural land management (IALM). A core feature is its SOC-centric design, treating increases in soil organic carbon as a primary removal component.

VM0042 can credit (i) SOC stock increases (carbon removals) and (ii) reductions in CO₂, CH₄, and N₂O emissions associated with agricultural activities. SOC is a mandatory carbon pool and cannot be excluded as de minimis.

Eligible practices include reduced tillage, optimized fertilizer and water management, cover cropping and crop rotation, improved residue management, and improved grazing management, provided they represent material improvements over pre-project practices.